"AestheticsInMotion" (aestheticsinmotion)

"AestheticsInMotion" (aestheticsinmotion)

03/05/2019 at 21:36 • Filed to: None

6

6

35

35|

"AestheticsInMotion" (aestheticsinmotion)

03/05/2019 at 21:36 • Filed to: None | 6

| 35 |

I’m now banking with—wait for it—my cellular service provider. 6 weeks in and I’ve had no issues. Why? Because 4.00% APY on a checking account with no fees, and a slick user interface.

So my money is currently waterfall’d, as I like to think about it. The top pool is clocal hcredit union ecking account , with a high (7 ish %) rate on the first $500. Fill that $500 p ool, and have an automatic monthly transfer of the interest down into the next pool, which is T- Mobile money, earning 4.00% APY on balances up to $3000 . Fill that $3000 pool , and transfer the monthly interest to CIT bank saving which earns 2.45% APY without a maximum account balance.

3 pools. Each dollar earning the most possible without risk. I used to be absolutely terrible at saving, but GREAT at spending! Now, despite making less than previous years, I’m never worrying about money like I used to. I’m traveling somewhat frequently without issue, which I could never seem to afford back when I owned a successful, profitable small business. Going into the deep end of money management has really changed this stuff for me. And it’s FUN! To the point where I’m somewhat curious about finance related careers even... And as seems to be a reoccurring theme, I wouldn’t have gotten started down this path without you all.

Next step is to learn about investing, but I think I’ll save that for 2020. This year is still solidifying accounts, and getting my credit card portfolio to where I want it to be. Which.... I’m one card away from. Just need to wait a few months thanks to Chase’s cursed 5/24 rule.

Anyone else enjoy this stuff? Any questions about John Legeres foray into banking? Love him or hate him, it’s impossible to deny that the T-mobile CEO has had a huge impact on the mobile phone world. While the T- mobile Money account may not have the highest maximum (for the good rate at least), it’s still pretty crazy to see 4.00% in a checking account that doesn’t require rediculous hoops to jump through.

Here’s a link to a review.

!!! UNKNOWN CONTENT TYPE !!!

Dr. Zoidberg - RIP Oppo

> AestheticsInMotion

Dr. Zoidberg - RIP Oppo

> AestheticsInMotion

03/05/2019 at 21:40 |

|

I wish I had the gumption for this level of free dollars. I don't even use a cash-back credit card... I'm old and lame.

CarsofFortLangley - Oppo Forever

> AestheticsInMotion

CarsofFortLangley - Oppo Forever

> AestheticsInMotion

03/05/2019 at 22:00 |

|

Millennials, am I right?

|

CarsofFortLangley - Oppo Forever

> Dr. Zoidberg - RIP Oppo

03/05/2019 at 22:00 |

|

Dude, get on the cash back cc game. Free cash

Wrong Wheel Drive (41%)

> AestheticsInMotion

Wrong Wheel Drive (41%)

> AestheticsInMotion

03/05/2019 at 22:03 |

|

Now t mobile just needs to make a cell service that actually works everywhere... I had t mobile for a couple of years but I always had issues out in the sticks or traveling places. I’m doing much better on Straight Talk running on AT&T towers. Nothing could beat that $30 5gb plan T-Mobile has and the extra perks are nice. But service reliability is king to me. I get better speeds more frequently but the tradeoff is I'm paying $35 for 3gb.

|

Dr. Zoidberg - RIP Oppo

> CarsofFortLangley - Oppo Forever

03/05/2019 at 22:04 |

|

Ehhhhhhhhhhhhhhhhhhhhhhhhhhhhhhh

But buying less things probably nets more money than a little cash back don't you think?

|

CarsofFortLangley - Oppo Forever

> Dr. Zoidberg - RIP Oppo

03/05/2019 at 22:07 |

|

I put everything on my Visa, and my wife has a carbon copy of it. You spend a lot during the course of your day to day.

|

AestheticsInMotion

> Wrong Wheel Drive (41%)

03/05/2019 at 22:08 |

|

Fair. If they don't have service where you go, kinda doesn't matter what prices/services they offer. I do like that they give you a free signal booster if you want one. I had good service in my home already, but hey might as well boost it

|

AestheticsInMotion

> CarsofFortLangley - Oppo Forever

03/05/2019 at 22:09 |

|

I had a fancy dragon fruit this morning. W hat have I become....

|

AestheticsInMotion

> Dr. Zoidberg - RIP Oppo

03/05/2019 at 22:09 |

|

What if you bought less things AND earned cash back/rewards on those things?

HammerheadFistpunch

> Dr. Zoidberg - RIP Oppo

HammerheadFistpunch

> Dr. Zoidberg - RIP Oppo

03/05/2019 at 22:27 |

|

i got over 650 back last year on my card. 4% on gas diving 2 vehicle that barely do teens for mileage

|

HammerheadFistpunch

> CarsofFortLangley - Oppo Forever

03/05/2019 at 22:27 |

|

this is what we do. run everything through it and pay it off

|

Dr. Zoidberg - RIP Oppo

> AestheticsInMotion

03/05/2019 at 22:34 |

|

Yeah, I know... I should do more things than the things I do.

Wobbles the Mind

> AestheticsInMotion

Wobbles the Mind

> AestheticsInMotion

03/05/2019 at 22:40 |

|

This is awesome! I’ ll do a post on Roth IRAs and a bit with investing as soon as I can t hat way, if you decide to start a Roth, then you can get in a bit of money for 2018 before the April 12th cut off. I like these pools and a Roth IRA is the next progression. Great stuff!

|

CarsofFortLangley - Oppo Forever

> HammerheadFistpunch

03/05/2019 at 22:41 |

|

Yep!

|

AestheticsInMotion

> Wobbles the Mind

03/05/2019 at 23:02 |

|

Please do! Either that or a CD was going to be my next step

MrDakka

> AestheticsInMotion

MrDakka

> AestheticsInMotion

03/05/2019 at 23:25 |

|

Just make laddered CDs if you're risk averse

R3d Cypher

> AestheticsInMotion

R3d Cypher

> AestheticsInMotion

03/05/2019 at 23:25 |

|

OK OK I think I understand this. The first one nets $35/month in interest holding $500 . This gets dumped into the second that earns in total $121.40 per month holding $3000 (Which meets the min of Chases $100/month or $25K balance req) Soo $ 1492.49 of essentially free cash after 1 year compounting at 2.45% APY. The total to get started is essentially $3500. This is pretty neat.

facw

> AestheticsInMotion

facw

> AestheticsInMotion

03/05/2019 at 23:37 |

|

CDs probably aren’t worth the bother. It’s good to have a couple months expenses in fairly liquid things, so your waterfall is not bad at all for that. But ultimately you want better returns, keep in mind you are losing ~2-3% to inflation, so only the 7% is “good”, though the others are certainly better than keeping it under the mattress (where you’d lose money to inflation).

Best thing to do once you have enough in the bank to cover your expenses including small emergencies, is to first put things into a diversified mutual fund with low overhead in an IRA, Roth IRAs are better than traditional for most people, but it’s worth looking at both (you won’t be able to touch the money for a long time without penalty, but you’ll need money then, and the tax benefits are good). If you can max those out, it makes sense to set up an auto purchase for a similar fund (maybe not entirely the same, to provide more diversity), just in a normal account. That money can be used for anything, but keeping it in a mutual fund means it will likely grow much faster than inflation (and you can still usually sell within a few days if you end up needing it in a hurry) .

For someone your age, almost all your investments should be mutual funds made up mostly of stocks. CDs, Bonds, and money market accounts may be safer, but you need to balance the risk that they won’t make enough money. Generally the idea is to invest heavily in stocks if you don’t have likely near term needs, and then start transitioning to more stable investments as you come up situations where you might need to sell (i.e. planning to buy a house, or preparing for retirement).

BeaterGT

> AestheticsInMotion

BeaterGT

> AestheticsInMotion

03/05/2019 at 23:39 |

|

I’m so confused. I mean it’s a cool idea , but T-mobile?

|

AestheticsInMotion

> BeaterGT

03/06/2019 at 00:03 |

|

Yeah, don't ask me. They've done a lot of strange things in the last few years, but with a rate like that I'm not asking too many questions

|

Wrong Wheel Drive (41%)

> AestheticsInMotion

03/06/2019 at 00:21 |

|

I've always just used wifi at home, Google voice works wonders to make it a seamless transition. I only care about cell reception while flying places or hiking or driving wherever. That's when I need it most and if I spend enough time at home I burn through barely a GB of data in a month. Maybe t mobile works decently out here on the west coast? I only had them back in NJ and everytime I went exploring in PA or in the northeast i was out of cell contact entirely, stuck with maybe 2g at best. They're also constantly improving so there's that. Definitely would go back just for that $30 plan but it's splitting hairs for that price point anyways.

|

AestheticsInMotion

> Wrong Wheel Drive (41%)

03/06/2019 at 00:33 |

|

I do find it interesting to see how different usage patterns can be. For example, I don’t have internet service, I just pay $50/month for unlimited data (they say it slows down after 55GB, but I go over that most months and still have good speed so...) on T- mobile and use a mobile h otspot for the rare moments when I can’t do something on my phone. Although I do kind of want to get back into gaming so I might need to rethin k this....

They seem pretty good on the west coast. I occasionally lose service on hikes that are deep in the mountains, but I think my friends with other providers do as well? My only real complaint is with the customer s ervice, but even there they're much better than my last provider, Verizon

|

AestheticsInMotion

> facw

03/06/2019 at 00:40 |

|

So what would be a good place to start with the mutual funds comprised mostly of stocks? That all sounds great, but I've yet to even dip my toes into stocks, and from the outside looking in it's a bit.... Intimidating

|

Wrong Wheel Drive (41%)

> AestheticsInMotion

03/06/2019 at 00:49 |

|

Ahh thats a pretty neat way of going about Internet I guess. That is definitely more affordable than my cell plan plus home Internet and I doubt Spectrum is any faster anyways! But between my girlfriend and I running multiple phones, laptops, and then the chrome cast and PS3, mobile Hotspot would not work very well lol.

|

AestheticsInMotion

> R3d Cypher

03/06/2019 at 01:45 |

|

That’s what I thought at first too, but those numbers are actually per year, not per month. So more like $ 150 per year, which is a lot less noteworthy. Still, it all adds up and once I start getting more money I'll be able to make this work on a larger scale, to the point where the interest payouts are actually pretty meaningful! Small steps

|

AestheticsInMotion

> MrDakka

03/06/2019 at 01:47 |

|

I'm considering that. It's not so much that I'm risk-averse, I'm just not knowledgeable enough yet to choose what risks to take, so until I get to that point I'll stick with the safer options.

|

facw

> AestheticsInMotion

03/06/2019 at 02:20 |

|

This may be a little complicated, but let me try to give you a highish level overview.

In general there are a few important concepts for small investors dealing with stocks:

Mutual funds: Mutual funds are made up of stocks of many companies. The fund’s manager picks these stocks, either actively, looking for the best deals, or by trying to match the composition of an index like the S&P500. This is better for most investors than picking stocks directly because you really are unlikely to match the performance of someone who does this full time for their job. Also transaction fees for frequently buying and selling greatly eat into the profits of day trader types. Mutual funds are usually intended as buy and hold type investments. Sometimes you’ll see the term ETF (exchange traded fund), which are pretty similar, it’s just a matter of how they are bought and sold)

Expense ratios: This is how much the fund spends annually on overhead. The cheapest index funds can do this for about 0.02 %-0.05% which is basically nothing. Actively managed funds will be more expensive. This doesn’t make them inherently worse, because if that extra expense translates into more profit, then it’s a win all around, but even for professionals, beating the market is hard, so funds with a 2% expense ratio are going to have a very hard time. In general you should look for funds with low expense ratios.

Dollar cost averaging: This is basically the idea that timing the market to buy low is hard, so for the long term investor it is better that the just invest periodically (usually once or twice a month), to make sure that they never miss the low. It also means you’ll hit the high, but you shouldn’t be too worried about that, the current price always reflects what investors feel is right, so it should never be a terrible deal. What you want to avoid is missing the low, and then investing everything at a high.

For my funds I mainly use Vanguard, which is a well regarded institution known for low fees. There are other choices of course so look around, but Vanguard’s no a bad place to start.

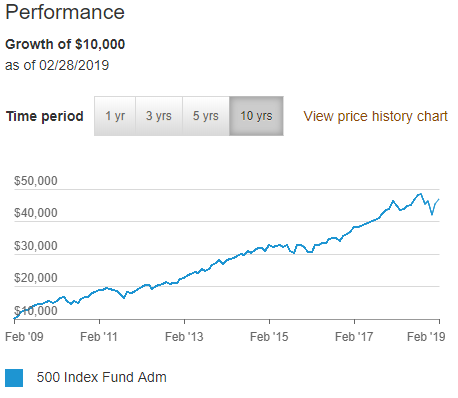

There will be lots of fund choices, from basic index funds to funds targeting specific industries or categories, and then on to actively managed stocks (costs more due to the overhead of having someone picking stocks ). Vanguard (and many other traders) even have funds targeted at specific retirement dates, that will automatically chang ing from aggressive to conservative investments as retirement gets closer. You can see a list and compare past performance. Here’s what that looks like on Vanguard:

https://investor.vanguard.com/mutual-funds/list#/mutual-funds/asset-class/month-end-returns

For normal investments, you should probably be most interested in the Expense R atio and the 10-year returns (past returns don’t guarantee future performance, but they help to understand what you are looking at). Note that the since inception numbers may be a bit weird since they could be less than 10 years old, or they could have been founded at a peak or valley making things look weird. The 10 year provides a more apples to apples comparison. The expense ratio is how much it costs to administer the fund so you’d subtract that from your annual returns along with inflation to see your actual return. Y ou might pay taxes as well, but not for a Roth, and most taxes you pay are paid when you sell rather than when it’s just sitting there (for non-Roths, you pay taxes on dividends, distributions from the company to shareholders, but those are small, most profit comes from the increasing price of shares, which are taxed as capital gains when you sell).

Some of these are targeting specific things for tax purposes or whatever, but you’ll mainly see fund divided into two dimensions:

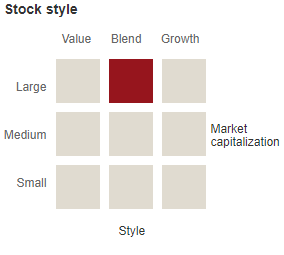

Small, Medium, and Large refer to the company size (or rather how much the all of the company’s stock is worth), Large companies are more stable, which makes them somewhat safer picks, and so large cap funds may be better as the core of your mutual fund portfolio, with good returns on lower risk.

Value, Blend, and Growth are characteristics of the stocks chosen. Value stocks are normally depressed companies that have a bleak looking future ahead of them. That may sound unappealing, but since everyone feels that way, their stock has already been hammered down so it may actually have appealing price-to-earnings, and could look quite cheap if the company rebounds. Warren Buffet has famously used a value investing strategy, so it’s worked for at least someone. Growth stocks are to opposite, they are stocks where earnings per share are probably low, but people still want to buy because they expect the company to have significantly better revenues in the future. Many tech stocks fall into this category. Blend is just a mix of the two. It’s possible to make money with either approach, but again, for the core of your portfolio, a blend is probably appropriate since you minimize the risk of either strategy failing badly.

You can also get a more detailed look at what you would be buying by looking at the fund’s prospectus. For example here is one of Vanguard’s simplest funds (this is basically just trying to hold stocks in the S&P 500) : https://investor.vanguard.com/mutual-funds/profile/VFIAX

Anyway I’m skipping a ton of stuff here, so if you have questions let me know. But the basic process looks like this:

Find a broker (Vanguard, T. Rowe, Charles Schwa b, etc.)

Decide if you are going to set up a Roth IRA, a T raditional IRA, or just a normal non-retirement account.

Tie your account with your bank. This is done by the normal routing number method so you can seamlessly transfer funds back and forth (often mutual funds will delay a few days to discourage rapid buying and selling, which increases their costs)

Save up for the initial investment (again to keep costs under control, they want you buying a big chunk at once) , many basic funds require $3000, while other funds can have requirements in the 10s of thousands or even millions. Some funds will offer lower expense ratios if you put more in.

Buy the fund or funds you want.

Set up automatic payments so that you can keep buying whatever you can afford over time, instead of lump sums. Normally contribution minimums are waived for automatic deposits. You can stop these at any time if money becomes tight.

Step back and see how much difference it makes to have strong return:

Note: I rewrote this a couple times, so if there’s stuff that makes no sense, it probably used to?

|

AestheticsInMotion

> facw

03/06/2019 at 02:48 |

|

Wow. Thank you so much for that, I know how taxing it can be to order your thoughts and then try to get it all down on kinja. I really do appreciate the help. I think I'll make it a new goal to get started with this during the summer.

|

facw

> AestheticsInMotion

03/06/2019 at 02:58 |

|

It’s definitely worthwhile if you can put aside the cash.

|

AestheticsInMotion

> facw

03/06/2019 at 03:25 |

|

So I think I understand the dollar cost averaging and why you want to invest somewhat frequently to even out the peaks and valleys so to speak, but how does that work with the presumably much larger single initial investment? Wouldn't it be entirely possible for that large sum to go in during a peak?

|

facw

> AestheticsInMotion

03/06/2019 at 03:47 |

|

Yep. You do want to time that if you can. For example, I put $10000 into something last November, and waited until the market had basically wiped out its gains for the year, which wasn’t bad, but if I had waited for the “Oh shit, that moron is going to break the economy over his stupid wall” moment in late December, I could have bought at 20% less , and made a few thousand more on the rebound.

Still it’s hard to hit those exact moments, had it gone up instead, I might have cost myself a bunch that way. As I noted, the good news is that the price you get is always what the market thinks is “right” at any given moment, so if it’s wrong, it fooled a lot of people who are in theory smarter than you. That said, I often do try to look at recent performance and buy when it is down a bit from recent highs. This is complicated because the mutual fund may take a few days to process you purchase (this lets them discourage day trading, bulk purchases so they are cheaper, use your money to pay off someone who wants to sell, so they don’t have to buy or sell the underlying stocks, or just skim a little interest off holding your money for a few days). So basically your best bet is to just try to find a local minimum and hope to get close enough, instead of trying to wait for minor crash or whatever. In the long run, it hopefully doesn’t matter too much.

nerd_racing

> CarsofFortLangley - Oppo Forever

nerd_racing

> CarsofFortLangley - Oppo Forever

03/06/2019 at 08:02 |

|

I’ve been thinking about the Amazon card. I hear their cash back program is one of the best.

|

R3d Cypher

> AestheticsInMotion

03/06/2019 at 17:32 |

|

Yeah it seemed really really high. I thought it may have been per year.

|

AestheticsInMotion

> facw

03/06/2019 at 20:42 |

|

Still have a couple of questions! Hope I’m not bugging you, just seems like a really good opportunity to learn from someone!

Let’s say I decided to start out similarly to your example above, putting $10,000 as an initial investment into Vangaurd’s 500 index f und a dmiral class.

What type of account would I want to have that fund go into? A Roth IRA opened through Vanguard? Would the $10,000 be too much because it counts towards the yearly limits for Roth IRAs? Or am I missing something altogether?

|

facw

> AestheticsInMotion

03/06/2019 at 21:01 |

|

So the yearly limit on Roth IRAs is currently (I think) $6,000 per person. So normally you wouldn’t be able to drop that in all at once. However, you are allowed to make a 2018 contribution up until tax day, so if you wanted to, you could make a $6000 2018 contribution, and a $4000 2019 contribution to get your $10000 in. Just to quickly clarify the account options:

Roth IRA: You put in after tax money, but it is then allowed to grow tax free (which is quite good) . This is a retirement account so until you are 60 (IIRC) you can’t withdraw money without paying a penalty (10%?). There are a few exceptions that let you withdraw early.

Traditional IRA: You put in pre-tax money, but have to pay taxes on earnings. This makes sense for some people, but I think for most the Roth is likely to be a better deal (obviously this is effected by what people qualify for, and what happens to tax policy down the road). Like the Roth, I believe it has an early withdrawal penalty.

Non-retirement account: Just a standard account to invest for whatever the future may have in store. No special tax benefits. You put in after-tax money, and are taxed on dividends as they are earned, and capital gains when you sell. Obviously no penalties for selling at any point (some funds make you wait a short time after purchasing to sell from that purchase, though if you make a $100 recurring investment, it would only be that $100 that would be temporarily blocked, not that whole account).

If you are looking for an S&P500 account, take note that Charles Schwab has been advertising a fund with a 0.02% expense ratio: https://www.schwab.com/public/schwab/investing/accounts_products/schwab_index_funds_etfs

That’s super small (it may even be a loss leader in the hope that you’ll invest with other more expensive accounts). On the other hand, Vanguard’s is cheap enough that it shouldn’t make a huge impact either way, I haven’t bothered to move my account over to get that lower rate (it is possible to shift money from one IRA to another, or to change funds within an account). Something you can look into and decide what you’re most comfortable with.